How Does Blockchain Technology Work? A Comprehensive Overview

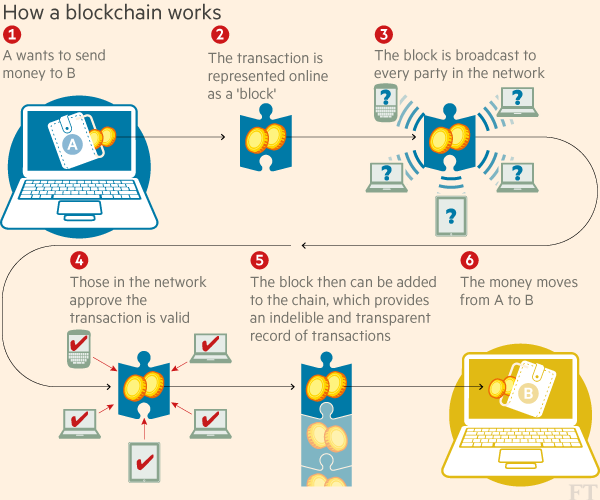

Blockchain technology operates as a decentralized digital ledger that records transactions across multiple computers. This ensures that the recorded transactions cannot be altered retroactively without the alteration of all subsequent blocks and the consensus of the network. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data, which is secured through cryptography. As a result, blockchain provides transparency and security, making it an ideal solution for various applications such as finance, supply chain, and healthcare. For a more in-depth understanding, you can check out this Investopedia article on blockchain fundamentals.

The operations within a blockchain network typically involve three key components: nodes, consensus protocols, and smart contracts. Nodes are individual computers participating in the network, validating and storing the blockchain's data. They communicate using a consensus protocol, which determines how they reach an agreement on the validity of transactions. Popular consensus mechanisms include Proof of Work and Proof of Stake. Additionally, smart contracts are automated programs triggered by specific conditions, facilitating self-executing agreements without the need for intermediaries. To explore these concepts further, consider reviewing the Ethereum Foundation's guide on blockchain technology.

The Benefits of Blockchain: Why Everyone is Talking About This Digital Ledger

The benefits of blockchain have sparked significant discussions across various industries, as this revolutionary technology offers numerous advantages that extend beyond cryptocurrencies. One primary benefit is transparency; all transactions are recorded on a public ledger, making it nearly impossible to alter any information without consensus from the network. This characteristic not only fosters trust among users but also enhances security, reducing the risk of fraud. Additionally, blockchain technology can streamline processes by automating tasks through smart contracts, which execute predefined actions when certain conditions are met. For more insights, check out this article on Forbes.

Moreover, blockchain technology promotes decentralization, eliminating the need for intermediaries in many transactions. This reduces costs and increases transaction speed, which is especially valuable in industries like finance and supply chain management. Users gain greater control over their data, ensuring that personal information is shared with consent and minimizing the risk of data breaches. As the world increasingly shifts towards digital solutions, the significance of blockchain cannot be overstated. To understand its impact further, visit IBM's blockchain guide.

What Are Smart Contracts and How Do They Revolutionize Blockchain Transactions?

Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They reside on a blockchain, which is a decentralized ledger that enables transparent and tamper-proof transactions. When certain pre-defined conditions are met, smart contracts autonomously trigger actions, such as transferring funds or executing agreements without the need for intermediaries. This technology not only enhances efficiency but also reduces costs associated with traditional contract enforcement. For more about smart contracts, you can visit Investopedia.

The impact of smart contracts on blockchain transactions is nothing short of revolutionary. By automating and securing the transaction process, they eliminate the risks of human error and fraud, promoting trust among parties involved. Moreover, smart contracts can facilitate various applications across industries, such as finance, supply chain, and real estate, streamlining operations and improving transparency. As the adoption of blockchain technology increases, understanding smart contracts becomes crucial. For deeper insights, check out IBM’s Blockchain resources.